Accessibility Links

September 2020 market review: South Africa

The devastating impact of the Covid-19 lockdowns echoed in key data releases in September. Read all the details in our market review.

Care and maintenance

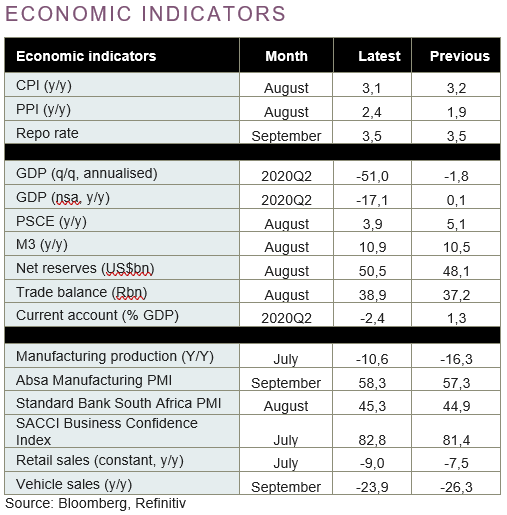

Unemployment data showed 2,2 million people lost their jobs, while second-quarter GDP declined by -16,4% over the quarter (-51,0% quarter-on-quarter, annualised) – a dire state of affairs and one that has focused the minds of stakeholders across different spheres of the economy. Under the auspices of National Economic Development and Labour Council, or Nedlac, business, labour and government came together on an economic recovery plan for the country. Data for the third quarter already shows improvement from this low base and will be further supported by the country moving to level 1 restrictions. But more intervention is required, and the country now waits for cabinet approval (and implementation) of the economic recovery plan.

With this backdrop, many investors struggle to see why SAA should remain a priority and deserve a further R10,4 billion to support rescue efforts. While government has committed to the moneys, finding this in a fiscally neutral manner has proven difficult and has resulted in the entity being placed under ‘care and maintenance’ by business rescue practitioners.

After delivering 300 bps of interest rate cuts over 2020, the South African Reserve Bank opted to keep rates on hold at the September meeting with a vote of three to two.

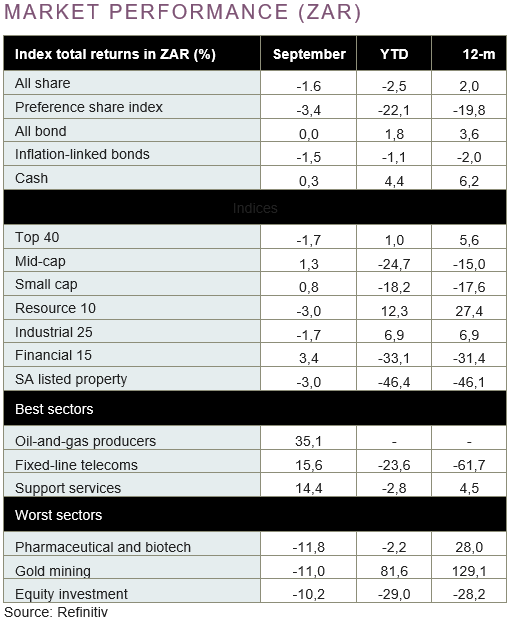

Fiscal concerns weighed on local nominal bonds in September, with the All Bond Index returning -0,05%. Bonds still outperformed other asset classes over the quarter, returning +1,5%.

Property companies are reporting an improvement in footfall as lockdowns have eased. The sector, however, continued to trade under duress, with the property index losing a further -3,0% over the month and -14,1% over the quarter.

With the prominence of technology company Naspers/Prosus in local indices, the FTSE/JSE All Share traded down -1,6% over the month, in line with global markets and technology counters, bringing the quarterly return to a modest +0,7%. The headline figures, however, hide a multitude of trends. Domestic retailer Shoprite and bank Capitec delivered +25,7% and +24,2% respectively over the month despite the tough backdrop and financial results, highlighting the weak expectations that were priced in. Small and mid-size companies continued to stage a recovery, gaining +3,5% and +1,3% respectively. Despite losing some ground in September, resources added +5,7% over the quarter and with 12-month returns at +27,4% has been one of the big drivers of the recovery in the local equity markets.

Want to know more? Here's what to do:

- Contact your wealth manager or stockbroker.

- To find out more about our investment offering, click here.

- If you're interested in what we can offer you, we would love to hear from you. You can contact us on 0860 111 263, or complete an online contact form.