Accessibility Links

August 2020 market review: South Africa

South Africa eased to lockdown level 2 in August, reinstating tobacco and alcohol sales and providing the tourism industry with a welcome reprieve. Read more in our latest market review.

Level 2

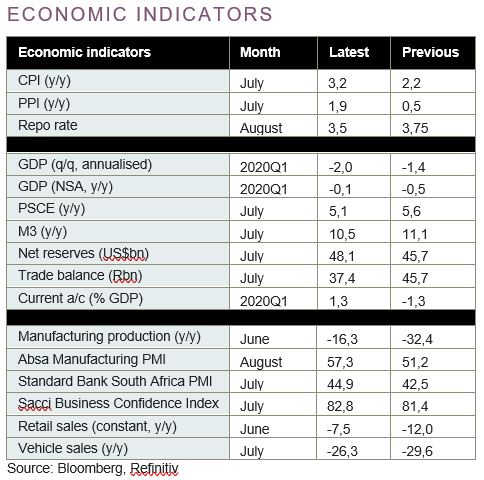

South Africa eased to lockdown level 2 in August, reinstating tobacco and alcohol sales and providing the tourism industry with a welcome reprieve by permitting interprovincial travel. Activity indicators have recovered from a low base, although the pace has slowed since the start of the third quarter. The easing of regulations will aid the recovery already underway, even as continued load-shedding weighs on the economy and sentiment.

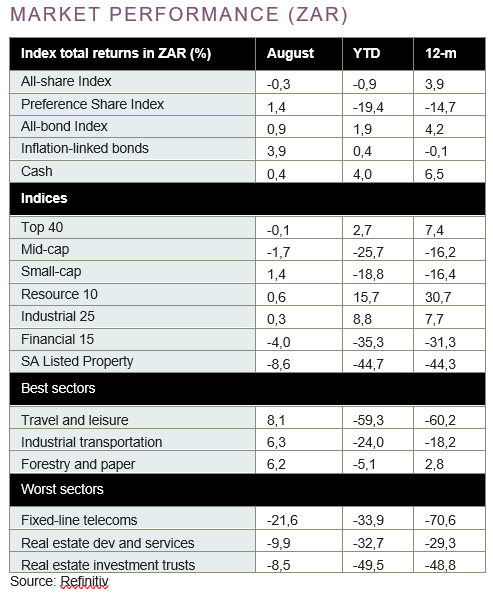

After tracking below the South African Reserve Bank’s target range of 3% to 6% in the midst of the pandemic, local inflation increased to 3,2% yoy in July. The monthly jump was largely driven by an increase in fuel costs due to a higher oil price and annual increases in municipal and utility costs, including water and electricity tariffs. Inflation-linked bonds benefitted from the reflation underway, returning +3,9% over the month. Local nominal bonds delivered modest returns, with the All-bond Index returning +0,9% in August.

Property counters continued to trade under duress, with the property index losing a further 8,6% over the month and bringing 12-month returns to a devastating -44,3%.

Poor trading conditions and the threat of structural change have seen property valuers take a more cautious stance, with financial results revealing meaningful impairments to property asset values.

The FTSE/JSE All-share returned -0,3% over the month, weighed down by financials while resources took a bit of a breather. Small-cap counters (+1,4%) outperformed large and mid-size companies as regulations were eased and the rand appreciation provided a tailwind.

Banks traded down over the month (-3,6%) as half-year results revealed the harsh impact from the current economic and health crises. Estimates and provisioning for credit impairments exceeded that of the global financial crisis. Although accounting requirements (International Financial Reporting Standards) result in more conservative assumptions for bad debts, the overall picture was still grim. In line with SARB guidance, none of the banks declared a dividend. In August, PSG Group distributed around 28% of their stake in Capitec to shareholders to unlock value for shareholders. While Capitec traded down alongside other banks over the month (-5,6%), PSG Group gained 27,1% as investors sought to capitalise on the unbundling.

It is a worthwhile reminder to keep an open mind – and that value can be unlocked – even at the most difficult of times.

Want to know more? Here's what to do:

- Contact your wealth manager or stockbroker.

- To find out more about our investment offering, click here.

- If you're interested in what we can offer you, we would love to hear from you. You can contact us on 0860 111 263, or complete an online contact form.