Accessibility Links

May 2020 market review: South Africa

South Africa entered lockdown level 3 at the start of June. This marks the full or partial return of business. Read more in our latest market review.

Level 3 – proceed with caution

After a noisy and somewhat clumsy transition, South Africa entered lockdown level 3 at the start of June. This marks the full or partial return of business activity for much of the economy with an estimated 8 million employees returning to work. This is a positive for the economy even as infection rates continue to escalate, especially in the so-called regional hotspots. Preparedness remains the focus, but the inevitable peak in active cases is yet to come and may again illustrate the complexity of the balancing act between lives and livelihoods.

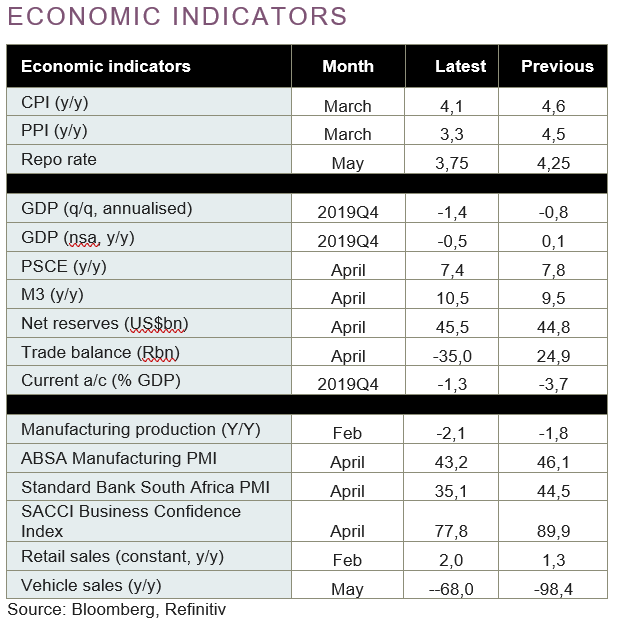

The future of SAA remains uncertain, with ongoing delays in the business practitioners’ proposals. Finance Minister, Tito Mboweni, will table a special adjustment budget on 24 June, which no doubt also has to address the thorny issue of support for SOEs. Manufacturing surveys and monthly vehicle sales data suggest a recovery is underway but confirms an economy that was struggling before the Covid-crisis and is still operating well below capacity. Reforms and a reinvigorated focus on economic growth have never been more pressing and will be key to the momentum of any recovery.

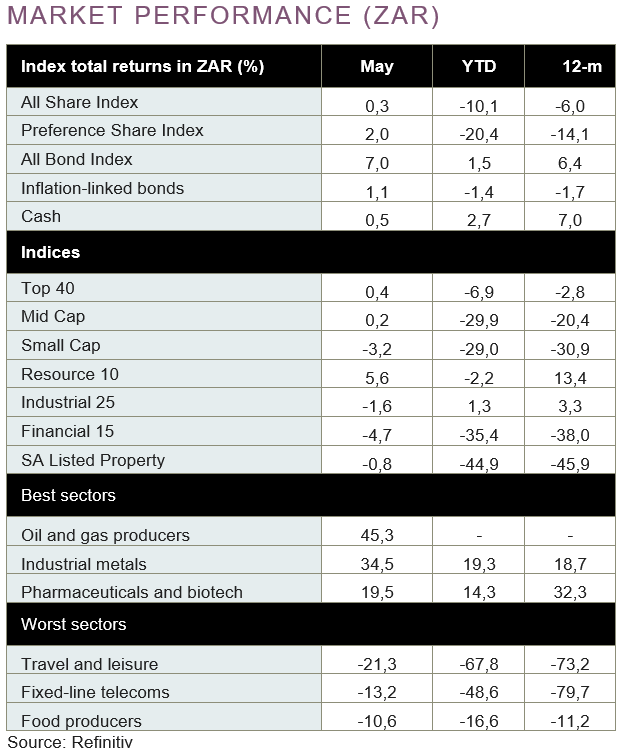

In line with market expectations the SA Reserve Bank cut interest rates by a further 50 bps, with a vote of 3:2, with two members favouring a 25 bps cut. This supported local bond markets in their recovery, with the All Bond Index gaining +7,0% in May and bringing the 12-month returns firmly into positive territory at +6.4%.

After a strong recovery in April the FTSE/JSE All Share Index flatlined in May, ending the month up by only +0,3%. Feedback from company results confirmed a lacklustre economic backdrop in the first quarter, worsened by load-shedding and the first glimpses of the meaningful impact of the nationwide lockdown. Cash preservation has therefore been prioritised, with dividends across several corporates cut, delayed or suspended. Domestic companies, financials and consumer-led sectors traded under pressure, while most of the positive momentum over the month can be ascribed to moves in industrial metals (+34,5%) and a stronger currency. Property counters gave up some of the previous month’s gains, with the sector weakening -0,8% over May. Most property companies are looking to preserve cash in the face of an uncertain return of trading and consumer activity, withdrawing or moderating distribution guidance for the time being. Although this is prudent, the lack of income generation may continue to weigh on sector valuations and investor appetite.

The recovery of markets has been swift but incomplete, and risks remain – we proceed with caution.

Want to know more? Here's what to do:

- Contact your wealth manager or stockbroker.

- To find out more about our investment offering click here.

- If you're interested in what we can offer you, we would love to hear from you. You can contact us on 0860 111 263 or contact@nedbankprivatewealth.co.za, or complete an online contact form.