Accessibility Links

Mounting credit rating pressure

Credit ratings and your portfolio

It would be an understatement to say that South Africa in 2017 has been eventful. It has been a year that saw cabinet reshuffles, an outcry from civil society, and #Guptaleaks. Corruption allegations, both old and new, implicated politicians and private sector organisations. It has also been the year in which the multi-year overhang from credit ratings agency concerns culminated in credit ratings downgrades for South Africa.

Although the timing of ratings agency actions may often take the market by surprise, ratings downgrades seldom come out of the blue. Typically, ratings actions are a lagging indicator. They tend to be a consequence of the deterioration (or improvement) of key metrics that indicate credit worthiness to a lender. Continued deterioration (with little intervention or action) that introduces heighted uncertainty and a further threat of deterioration (such as change in policy following a change of leadership) often serve as catalysts for action. And so it was…

The aftermath of the first cabinet reshuffle

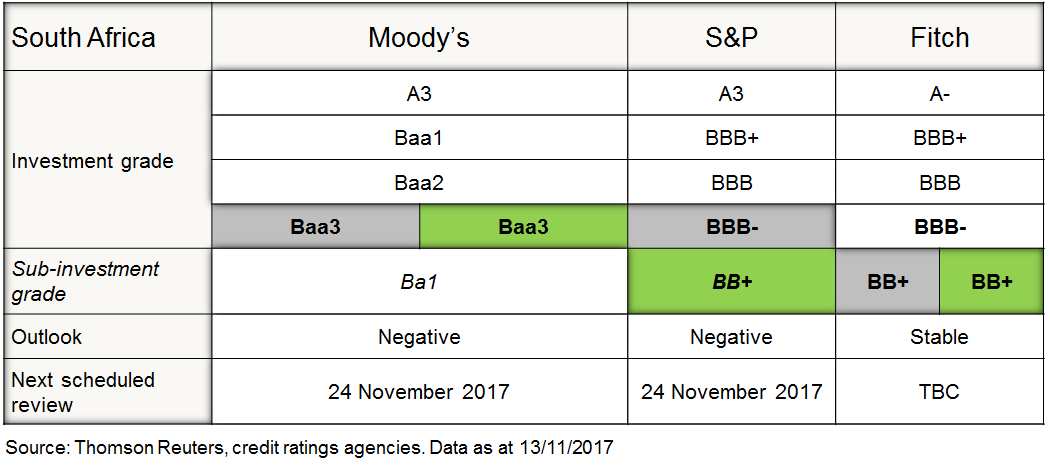

In an out-of-schedule review on 3 April 2017, ratings agency Standard & Poor’s Global Ratings (S&P) lowered South Africa’s local and foreign currency debt rating by one notch and left the outlook on both debt instruments negative. The foreign currency debt now sits at a sub-investment grade rating of BB+, while the local currency debt rating is one notch above high-yield status at BBB-. S&P’s primary reasons for the downgrades were elevated political risks and likely policy shifts that could ‘undermine fiscal and economic growth outcomes more than we would currently project’.

On 7 April 2017, Fitch Ratings (Fitch) followed suit, downgrading the country’s foreign and local debt to sub-investment grade, with a stable outlook. They cited many concerns, but essentially marked South Africa down in two areas:

- Macroeconomic Performance, Policies and Prospects – weak growth prospects, with repercussions for public finances

- Structural Features – deterioration in governance standards, particularly related to state-owned enterprises (SOEs)

Moody’s Investors Service (Moody’s) placed South Africa on review for a downgrade on 3 April 2017, but chose to wait until June before taking action. They downgraded South Africa by one notch, with a negative outlook. This left both local and foreign currency debt one move away from sub-investment grade status.

Below are the current long-term ratings for both local currency (LC – shown in grey) and foreign currency (FC – shown in green) bonds from all the ratings agencies.

Why do credit ratings agencies matter?

The three major global credit ratings agencies are S&P, Moody’s and Fitch. Globally, investors use ratings from these organisations as an independent assessment of the creditworthiness of an issuer, whether this is a country, corporate or the credit quality of an individual debt instrument. This is like the assessment that a bank will do about an individual when they apply for a loan or for credit. Each organisation has a distinct framework to assess the ability and willingness of a creditor to meet its financial obligations, however, there is a broad common framework we can refer to. Factors that ratings agencies consider include:

Ratings aim to be forward-looking in nature, although ratings agencies use historic data to inform part of their analysis. Assessments of strength or weakness are typically absolute in nature, rather than relative to a peer group – although they may compare similar entities and instruments in a category.

Ratings aim to be forward-looking in nature, although ratings agencies use historic data to inform part of their analysis. Assessments of strength or weakness are typically absolute in nature, rather than relative to a peer group – although they may compare similar entities and instruments in a category.

Why does this matter? Credit ratings affect one’s ability to raise money and the cost of doing so in local and foreign markets. A ratings downgrade signals increased risk to investors and lenders. This can cause negative sentiment, and an increase in the cost of capital, which in turn increases the cost of servicing the debt. This applies to the country, but also individual companies, as their ratings aren’t typically allowed to be higher than the country’s rating.

In addition, South Africa’s membership in certain bond indices (such as the Citi World Global Bond Index) is contingent on a minimum credit rating. A ratings downgrade may lead to South African bonds being excluded from these indices, which can force certain institutional investors such as retirement funds and passive index funds to sell their South African bonds.

For a while now, South Africa has been under scrutiny from credit ratings agencies. They have raised concerns related to weak economic growth, fiscal pressure and political and policy uncertainty. South Africa, SOEs and individual companies have raised funding in rands (local currency debt) as well as other currencies, such as the US dollar and euro (foreign currency debt). While South Africa can raise debt locally through several captive buyers, raising money offshore becomes increasingly more costly and difficult when our perceived credit quality deteriorates. In addition, local lenders may require more compensation to lend money to government, or may choose to stop lending to government.

Although improved trade conditions have helped this year, South Africa still relies on foreign investment to fund its current account deficit. (South Africa imports more goods, services and capital than it exports.) A downgrade increases the cost of this funding and weakens our ability to retain this funding option.

Global investors searching for yield in a low-return environment have found South African debt appealing, which has led to increased foreign ownership of local currency bonds. According to data from Treasury, this has reached historic highs of 41%, which means that a reversal of these inflows could have a material effect on bond markets, not only from a valuation point of view, but also for South Africa’s current account position.

Over time, the increased cost of servicing national debt and the cost of capital affects a wide range of companies, (especially banks) and consumers. We typically see the initial effects in the rand and bond yields. We then tend to see upward pressure on both inflation and interest rates. Over the long term, expensive debt and reduced inflows result in lower economic growth prospects, a negative spiral, which will affect all of us in South Africa.

Where are we now?

Finance Minister Gigaba delivered his maiden Medium Term Budget Policy Statement (MTBPS) on 25 October 2017. It will be remembered for its honesty about a deteriorating and challenging fiscal situation and the conspicuous absence of a corrective action plan or even proposal to mitigate the current state of events or consolidate our fiscal situation. The MTBPS left the market cold and the credit ratings agencies expressed renewed concern.

This has increased the possibility of further downgrades from as early as 24 November 2017, the next scheduled review date for S&P and Moody’s. While both agencies have expressed a desire to understand policy direction after the ANC Elective Conference in December 2017, they may well decide that the country has already deviated too far from the path and announce further downgrades before then. Their alternative would be to place the country on credit watch – to be resolved in three months, which would allow them time to assess future policy direction and the February 2018 Budget.

South Africa is represented in several bond indices through local currency bonds, which have not been downgraded to below investment grade, yet. For some of the indices, such as the JPMorgan (JPM) GBI-EM Investment Grade (IG) Index, one downgrade can lead to an exit, while other indices require two downgrades from specific entities. It may take a while for the process to unfold, but any further ratings downgrades will reduce already low confidence and cause investment outflows.

South Africa has already exited the JPM GBI-EM IG Index, but this only represented a small component of bonds held in these indices. The bulk of local currency bonds are held in the Barclays Global Aggregate Index and Citi World Government Bond Index (WGBI); the latter has the largest holding, at an estimated R100 to R120 billion.

South Africa has already exited the JPM GBI-EM IG Index, but this only represented a small component of bonds held in these indices. The bulk of local currency bonds are held in the Barclays Global Aggregate Index and Citi World Government Bond Index (WGBI); the latter has the largest holding, at an estimated R100 to R120 billion.

Although the credit ratings are symptomatic of structural challenges and lack of change, if it prompts significant investment flows, it could certainly intensify problems. It also takes time, often years, to rebuild to a credit rating upgrade.

How have we positioned client portfolios?

In January, we were witnessing green shoots emerge in the economy with the likely tailwind of receding inflation and further strengthening of global economic growth. After the March cabinet reshuffle, we decided that the domestic risks had increased and warranted a more defensive stance. Depending on client-specific circumstances, we generally recommend allocating more than the typical 25% offshore approach. The broad objective is to reach a 50/50 South African/offshore exposure over time. Increased international exposure offers diversification through wider investment opportunities, access to higher growth and better risk-adjusted returns, in addition to protection against single country and currency risks.

We have erred on the side of caution in our South African asset class positioning, favouring assets with more predictable return profiles and resilience against this difficult backdrop. Within risk assets, such as equities, we have retained focus on valuation and quality with a preference for companies that generate international earnings. We have been selective and more defensive in our bond exposure, preferring to be underweight debt instruments that are particularly sensitive to higher interest rates and selectively adding shorter-dated corporate paper where it made sense.

Ahead of a period that may bring with it increased volatility, client portfolios remain broadly balanced, taking risk where it is most appropriate and more likely to be well rewarded.

Nedbank Private Wealth Investment Team

21 November 2017