Accessibility Links

August 2020 market review: International

The global economy is recovering. Activity indicators are improving month-on-month from a low base as people return to work and more businesses reopen. Read our latest market review.

Summer surprises

The global economy is recovering. Activity indicators are improving month on month from a low base as people return to work and more businesses reopen. The reopening of economies was bound to lead to a resurgence in new Covid-19 cases. This premise has borne itself out, despite the warmer summer weather.

The pace of infection has once again accelerated across Spain, France and Germany, while holidaymakers returning to the UK from Europe arrived to a two-week quarantine. Thus far, the impact has been contained. But it serves as a reminder of the coming winter in the northern hemisphere and the risk of a more aggressive second wave of infections.

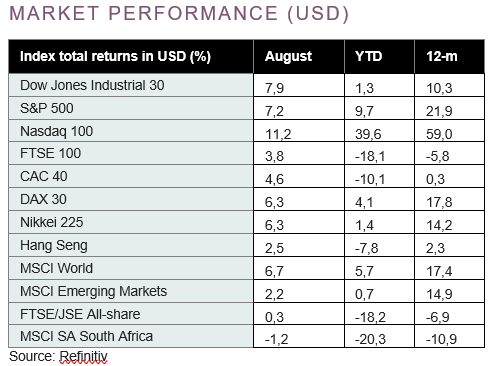

The second quarter earnings season delivered some staggering numbers – earnings came in better than market expectations. Although further fiscal stimulus in the US remains unresolved, this was not enough to put a dampener on market momentum. In addition, the US Federal Reserve’s message of lower interest rates for longer provided an added sweetener. This backdrop and vaccine optimism set the tone for further gains in market indices across the globe and a true summer bonanza for US technology stocks.

Leadership

The drive for global leadership, be it in technology, innovation, military capacity or economic growth and prosperity, has set the tone for every decade and crisis. One has to consider only the Cold War period and the space race to recognise similarities with some of the tensions playing out today.

The fight against Covid-19 has been laden with similar political pressure. In August, Russia became the first country to grant regulatory approval for the production and distribution of a vaccine, Sputnik V. Despite reassurance from President Vladimir Putin that the drug had passed all necessary tests, scientists have highlighted the absence of a large phase 3 clinical trial typically required as evidence that a drug is both safe and effective. In the US, the Food and Drug Administration has fast-tracked the approval of antibody treatment using blood plasma, despite sample sizes being smaller than is typical. Results will, however, be made public at each stage, which does provide for some scrutiny and transparency.

President Donald Trump continues to make proclamations, all while the regulators advocate for safe and sustainable solutions. Things are likely to heat up as the US elections approach, whether that be on US-China tension front or that of the race to provide a vaccine for Covid-19.

On average

Every year the city of Jackson Hole hosts the world’s central banking conference: the Jackson Hole Economic Symposium. This much anticipated event delivers current thinking on policy issues as well as an opportunity for central bankers to communicate with the market. The agenda for this year was filled with strategies deployed during the Covid-19 crisis, the threat of unemployment and new frameworks or tools for the future – given near-zero, developed world interest rates.

Following months of speculation, the US Federal Reserve confirmed a shift in policy. Their dual mandate aims to address both employment and inflation, with the inflation target set at 2%. A new, long-term strategy will aim for average inflation of 2%, which will enable periods where inflation will run above this level to compensate for periods running below this level. Essentially it is a more lenient approach to inflation and one that will see interest rates close to zero for longer. It is unclear whether other central banks will follow or even what the Fed’s mathematical definition of 'average' is. On average though, the odds of higher inflation in future may just have increased.

Want to know more? Here's what to do:

- Contact your wealth manager or stockbroker.

- To find out more about our investment offering, click here.

- If you're interested in what we can offer you, we would love to hear from you. You can contact us on 0860 111 263, or complete an online contact form.